Custom home building is the dream, isn’t it? You choose the layout you want, the design options you like, where you want to live, and everything is updated and new.

But how do you save enough to afford the cost of a custom home?

In this article, we share 10 of the best ways to save for a new home. When you break it down, the dream is attainable!

How to Save for a Custom Home

1. Set a Goal

How Much Do I Need for a New Home?

There is a lot that goes into the total cost of a new home, but as far as the upfront costs that are needed to get started, here’s what you should consider:

-

Cost of a Down Payment

-

Moving Expenses

-

Finishing Touches

-

New Furniture and Appliances

Learn more about each one and what to consider as you save.

Cost of a Down Payment

To determine how much you need for a down payment, talk with your family about what you want in a new home. How many bedrooms should it have? Do you want an office? What about an extra living room? A large backyard?

While all of this may seem preliminary, deciding what’s important to you from the beginning can help you narrow down the size and type of home you want to build.

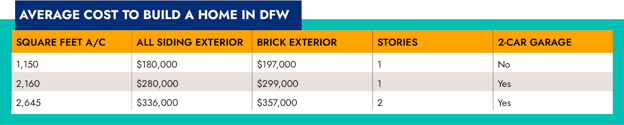

Below is a cost estimate of how much money you’ll need to build a custom home in Dallas-Fort Worth based on the square footage.

As we talk more about here, there are additional factors to consider that may increase this cost:

As we talk more about here, there are additional factors to consider that may increase this cost:

-

Options and upgrades you choose for your home

- Where you build and the cost of your lot

- The homebuilder you choose

You can also meet with a builder to learn more about their prices and how much you can expect to pay for the house you want. Once you have a rough estimate of how much your custom home will cost, you can determine how much you need to save for the down payment.

Most banks will require a 20% down payment for a construction loan, but some may only require as low as 5%, depending on the lender you choose. While you are still in the early stages of saving, you may want to reach out to a few lenders in the area to learn more about what they would require of you for the down payment.

Moving Expenses

While you won’t need to have the money saved right away for these expenses, it’s good to keep moving expenses in mind as you finish saving up for your down payment.

Moving expenses will include:

-

Hiring movers to move your furniture from one place to the next (and if you’re moving out of your home into a rental while you build, you’ll want to keep that cost in mind, as well)

-

Setting up the utilities at your new house

Finishing Touches

You also may want to set aside money for the finishing touches of your custom home. This could include:

-

Home security system installation and set up

-

Fencing or landscaping that wasn’t included in the custom home price

-

An outdoor kitchen you wanted to save for later

-

Adding a pool to the backyard

New Furniture and Appliances

Now for some of the fun stuff - new furniture and appliances.

Appliances are probably top of the list for a new home - new dishwasher, oven, microwave, refrigerator, and maybe even a washer and dryer if you’re looking to upgrade. Many homebuilders will include some appliances in the total cost of the home - like an oven, dishwasher and maybe even a microwave - so be sure to talk with your custom home builder about what's included in that total cost.

If you’re building a larger home than what you were in before, or you’re just looking to update your furniture, you may also want to budget for new furniture and home decor.

Keep in mind that you can also finance some of these things, as most of them - excluding the dishwasher, oven and microwave - won’t be needed until after you close on your new house.

2. Evaluate Your Spending

Where Is My Money Going?

Once you understand how much is needed for a down payment, start looking at your current spending habits and expenses.

Look at your bank account month over month and take note of any recurring payments.

Additionally, use a budget tracking app to track your spending habits, so you can see how much you usually spend on groceries, doctor’s bills, and entertainment each month.

After you have a clearer understanding of your spending habits, it will be easier to address this third step in the money-saving process: making cuts.

3. Make Some Cuts

What Monthly Expenses Need to Go?

This will be the quickest way to save money for a new home.

Once you have a better understanding of where your money is going, you can see where to make cuts. That subscription you signed up for a year or two ago that you don’t pay attention to anymore would be one such cut to make to your monthly expenses.

Then look at other things you can do to cut down on monthly costs:

-

Meal plan and cook at home more

-

Stick to your shopping list when you go to the grocery store

-

Think about where you shop. Could you shop at Walmart or Aldi to save money on groceries each month vs. going to Target or Albertson’s?

-

Collect and use coupons when you go grocery shopping. You can find a lot of great deals in each store’s mobile app.

-

Cancel cable and cut back on entertainment costs. Can you get rid of cable and just choose one or two streaming services to watch?

-

Reduce electricity usage. Switch your light bulbs to LEDs, turn off the lights when you aren’t using them, program your thermostat to only run at certain times, plan to do laundry just once a week.

-

Commute to work or other events to save on gas.

-

Maybe downgrade this year’s family vacation. Instead of a trip to Disney World, what if you went camping for the weekend or drove up to Silver Dollar City?

4. Create a Budget

What Will I Spend My Money on Each Month?

Next, it’s time to create a good budget. There are a lot of great tips and tricks for creating a budget, but you essentially want to think through the following categories:

-

Income. How much money do you earn each month?

-

Necessary Expenses. What are your monthly expenses? (i.e. monthly rent or mortgage, utilities, car payment, phone bill, medical expenses, grocery bills).

-

Other Expenses. What are some other categories that you want to keep in the budget? Entertainment? Extracurriculars?

-

Subtract Your Expenses from Your Income. Once you do this, you can see how much money you should be able to set aside and save each month.

5. Pay Off Debt

What Debt Can I Pay Down?

Another important piece of saving for a new home is managing your debt. Lenders don’t just care about whether or not you have enough money for a down payment; they also look at your debt-to-income ratio to determine if you qualify for a loan and how much money you qualify for.

Most lenders like to see a debt-to-income ratio of 45% or less. If you can trim down your debt while you’re saving, you’ll be in a good place for your construction loan application.

6. Open a Savings Account

Where Can I Put My Money as I Save?

Next, you’ll need a place to put the money you save. If you keep all of your money in a general checking account, it will be a lot easier to spend it rather than save it. Setting up a Savings Account or a separate Checking Account labeled “Savings” is a good way to set this money aside so you’ll have it when it comes time to apply for your loan.

7. Move Money into Savings

How Much Money Will I Put into Savings Each Month?

As you begin saving for a home, move that money into your Savings Account.

You can also try this fun budgeting strategy to boost your savings account:

-

Create a Checking Account labeled “Savings” and subsequent accounts for everything else:

-

Bills

-

Giving

-

Husband Spending

-

Wife Spending

-

-

Have your paychecks deposited into your account called “Savings”

-

At the start of each month, move a set amount of money into each of your accounts - Bills, Giving, Spending.

By following this strategy, if you make more money one month over another, your categories like “Bills, Spending, Giving, etc.” always receive the same amount, but your “Savings” category gets the rest.

As you consider how much money you need to set aside each month, look at your overarching goal and break it down into smaller goals. Dave Ramsey offers this great example for saving for a new home:

“Break down saving for a house into smaller steps. For example, saving a $40,000 down payment might feel impossible until you break it down into smaller monthly goals. If you pushed yourself to save $1,700 each month for 24 months, you’d hit that $40,000 goal.”

8. Utilize Retirement Funds

Could I Safely Pull from My 401(k) or Put Less Aside Each Month?

Please consider this piece of advice very carefully. This may not be advisable for everyone. If you are young and still a long way off from retirement, pulling from your 401(k) is not as risky as doing it when you’re older. It’s also not as risky to pull back (temporarily) from putting aside money toward retirement each month as you work to save for a house.

Just remember that if you do decide to pull from your 401(k), you may have to pay a fee to do so and you’ll want to put that money back as soon as you can.

9. Liquidate Current Real Estate Assets

Would I Make Money from Selling My Current Home and Renting While My Family Builds?

We talked before about the power of Instant Equity. If you already own a home, you might want to look into how much equity you have acquired from your home. Especially with how hot the market has been, you may be able to make a lot of money from your house by selling. In doing so, you could pocket that cash to use toward your down payment and downsize into an apartment or small rental house while you build your new home.

10. Take on Extra Side Jobs to Add to Your Savings

Are There Ways My Family and I Can Earn Additional Money to Help Us Save?

This is another tip that we’d recommend considering with caution. You don’t want to overwork or work yourself to death trying to save for a new home, BUT if you have the capacity to take on odd jobs to earn some extra cash, it’s a great way to put more money into your savings.

Maybe you’re a web developer and you could develop some websites for business owners you know, or maybe you really love to landscape and think you could offer that as a service on the weekends, or maybe you have a lot of stuff at home that you could benefit from selling (either in a garage sale or Craigslist or NextDoor).

There are a lot of side jobs you could try to earn some extra cash and increase your savings in the process.

Are You Ready to Get Started?

Request Pricing for Your Custom Home